National Dental Commission Bill, 2023 passed by the Parliament (GS Paper 2, Governance)

Why in news?

- Recently, the Parliament has passed the National Dental Commission Bill, 2023.

- It underscores the government's unwavering commitment to ensuring the highest standards of dental care for its citizens.

- The National Dental Commission Act 2023, will introduce a groundbreaking regulatory framework by establishing the National Dental Commission (NDC), which will replace the existing Dental Council of India (DCI) and repeal the Dentists Bill, 1948.

Key Highlights:

Constitution of National Dental Commission and State Dental Councils:

- The Act establishes the National Dental Commission and mandates the formation of State Dental Councils or Joint Dental Councils.

- This structure aims to decentralize authority and enhance effective regulation.

Three Autonomous Boards:

- The Act will empower three distinct Autonomous Boards: the Under-Graduate and Post-Graduate Dental Education Board, the Dental Assessment and Rating Board (DARB), and the Ethics and Dental Registration Board (EDRB).

- These boards will carry out specific functions, contributing to a comprehensive regulatory framework.

Fixed Tenure and Professional Development:

- The Act will introduce a fixed tenure for the Chairperson, Members, and Secretary of the Commission, with no possibility of reappointment.

- The NDC will emphasize promotive and preventive dental care services and will focus on fostering the soft skills necessary for career advancement among dentists and dental auxiliaries.

Industry Collaboration and Technological Innovation:

- Recognizing the importance of collaboration and research, the Act will encourage partnerships with industry and institutions to promote advancements in dental research.

- It also emphasizes the integration of cutting-edge technology into dental education.

Online National Register and Dental Advisory Council:

- The Act will provide for maintaining an online and live National Register of licensed dentists and dental auxiliaries.

- It establishes a Dental Advisory Council with representation from all States/Union Territories to ensure comprehensive insights and guidance.

Merit-Based Selection Process:

- Under the Act, the NDC will be led by a 'selected' Regulator.

- This entails the appointment of the NDC Chairman and Members through a merit-based selection process conducted by a Search–cum-Committee chaired by the Cabinet Secretary.

Collaborative Approaches:

- The Act will facilitate joint sittings with relevant statutory bodies, including the National Medical Commission, Pharmacy Council of India, Indian Nursing Council, National Commission for Indian System of Medicine, National Commission for Homeopathy, and National Commission for Allied and Healthcare Professions.

Fee Regulation and Constitutions:

- The Act will empower the Commission to frame guidelines for fee determination for fifty percent of seats in private dental colleges and deemed Universities.

- Additionally, within a year of the Act’s commencement, all State governments will establish State Dental Councils or Joint Dental Councils.

Way Forward:

- It is poised to usher in vital regulatory reforms in the dental education sector.

Consider setting up one exclusive shop for millets in every district, Panel to Centre

(GS Paper 3, Economy)

Why in news?

- Recently, the Parliamentary Standing Committee on Food, Consumer Affairs and Public Distribution gave recommendations with a view to give impetus to the consumption of coarse grains and millet-based food products.

- The United Nations has declared 2023 as the International Year of Millets.

Details:

- It recommended that the central government should consider setting up at least one shop initially selling exclusively millets and millet-based products in every district of the country, preferably by Khadi and Village Industries Commission, Tribes India, self-help groups especially run by women.

- This initiative will introduce the variety of coarse grains to the people at one place and will give them liberty to choose coarse grains as per their taste and choice.

Millets in PDS system:

- Earlier the committee had also suggested to the ministry that the beneficiaries of different schemes should be given the option to bundle millets along with wheat and rice within their entitled quantity.

- It reiterated in the new report that the government should explore the possibility of distributing millets in addition to rice / wheat under the Targeted Public Distribution System and other welfare schemes (Integrated Child Development Services and PM-Poshan), with a view to encouraging more states to opt for nutritious and healthy millets in combination with rice and wheat.

Initiatives taken by the Government:

- The Department of Consumer Affairs said it has drawn a roadmap to increase production / consumption / exports and branding of coarse grains / millets.

- Following this, the government was implementing the National Food Security Mission with the strategy of focusing on low productivity and high potential districts including cultivation of coarse grain and millets in rainfed areas, fallow lands and waste lands, and implementation of cropping system centric interventions.

Challenges:

- The government, highlighted the challenges in procurement and processing of coarse grains.

- The procurement of coarse grains as it relies on factors such as market price, climatic conditions (unseasonal rainfall, among others), stated the Union Ministry of Consumer Affairs, Food and Public Distribution.

- The primary processing of millets was the major challenge faced by millet farmers.

- To address this problem, the Union Ministry of Agriculture and Farmers Welfare is supporting rural farmers through 12 farmer-producer organisations (FPO) for the purchase of primary processing equipment, they said.

- This is being done with the financial support of NABARD, National Cooperative Development Corporation (NCDC), Small Farmers agri-business consortium (SFAC) and other state government agencies, the representatives added.

Millets production:

- There has been a marginal increase in sowing of millets in the ongoing Kharif season compared to 2022. This year, 16.42 million hectares area was sown under different coarse grains like jowar, bajra, ragi, maize and small millets.

- This was an increase of 1.09 per cent compared to 2022, when 16.24 million hectares was sown.

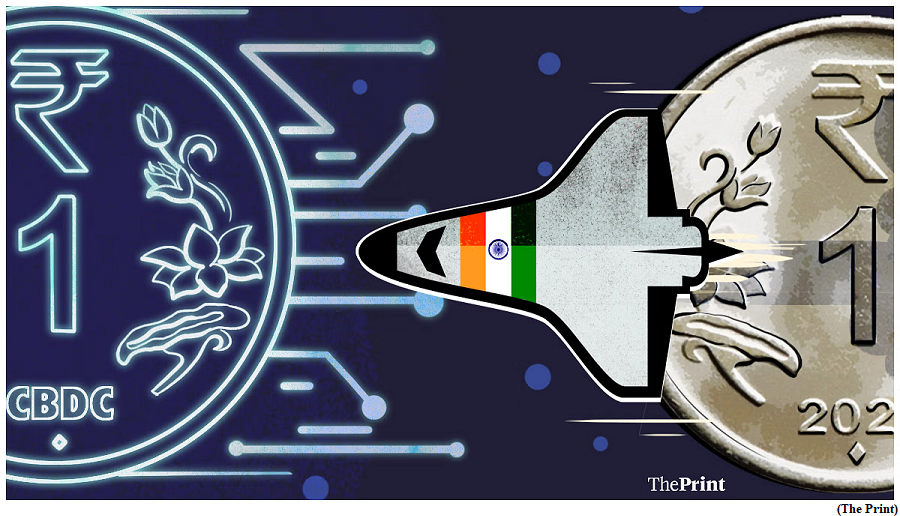

RBI wants to scale up e-rupee via UPI

(GS Paper 3, Economy)

Why in news?

- The Reserve Bank of India piloted a Central Bank Digital Currency (CBDC), the e-rupee, in November 2022.

- Now, the RBI aims to scale up CBDC usage through the popular Unified Payments Interface (UPI) platform, with a target of 1 million daily CBDC transactions by year-end.

Background:

- Finance Minister unveiled the introduction of CBDC during the February 2022 Union Budget presentation. Subsequently, the wholesale pilot commenced in November 2022, followed by the retail pilot in December 2022.

- As of June 2023, around 13 lakh users downloaded the CBDC wallet, with around 3 lakh vendors accepting payments in e-rupees.

- However, some experts claim that the goal is “far-fetched”, especially given a lack of awareness about the e-rupee and the limited number of banks that are participating in the pilot programme.

What is CBDC?

- CBDC refers to sovereign currency issued by a nation’s central bank, but existing digitally rather than as notes and coins.

- While they function similarly to private cryptocurrencies, they are positioned as ‘safer’ and serve as a medium of exchange rather than as assets.

- On the retail front, the pilot involves only 13 partnering banks, some of which include State Bank of India (SBI), Bank of Baroda, HDFC Bank, IDFC First Bank, and Kotak Mahindra Bank. These banks have provided a limited number of customers with an option to experiment with the digital rupee and be a part of the retail pilot.

- HDFC Bank is the first and so far, only bank that has introduced UPI scan codes for transacting in CBDC for select users.

How are CBDCs different from UPI and crypto?

- CBDCs are a type of digital money based on distributed-ledger technology similar to cryptocurrencies, but they function differently.

- And though CBDCs are similar to UPI in that they both use wallets to store digital currency, they differ in how they are issued and used.

- One major difference between CBDC and the existing UPI facility is that the latter requires a bank to facilitate the transaction.

- While transacting through CBDCs, the digital currency is debited from the sender’s e-wallet and credited directly to the receiver’s wallet. It skips the process of money being deposited in the bank accounts of customers.

- However, the issuance of CBDCs to retail customers involves transacting through a bank.

- The way the system works is that retail customers can use a wallet-based app from where they can raise tokens requesting the issuance of the CBDC. The request will be processed through the app and the partnering bank will then transfer the CBDC to the customer’s wallet.

How will scaling up CBDCs help?

- At a macro level, CBDCs offer an avenue to reduce the costs of printing, storing, and distributing physical notes. Printing currency constitutes a substantial portion of the RBI’s expenditure, reportedly amounting, for instance, to Rs 5,000 crore in 2021-22.

- In addition, the RBI also controls the cash circulating in the economy. The central bank cannot keep printing currency notes continuously on a large scale, as it would in the longer term, increase the purchasing power of consumers, diminish the value of money, and eventually lead to inflation.

- CBDC can help mitigate this risk by providing a more controlled way to inject money into the economy through the token system.

- Further, CBDC reduces the issue of counterfeit currency.

- RBI has said that with the digital rupee, the additional layer of banks would be subtracted from the system.

- In the current UPI payment system, when a user sends money to a merchant/user, the money gets debited from the sender’s bank account and then through UPI system, gets credited to the receiver’s bank account. The receiver cannot directly use the money without having to go through the bank.

Downsides of the digital rupee:

- The CBDC system suffers from some drawbacks, most notably the inability to accrue interest.

- Though CBDC is a digital currency and store of value, it does not yield interest in savings accounts. User cannot deposit CBDC in fixed deposits, or recurring deposits with banks as you do with the current currency. It can only be stored in the wallet.

- This factor serves as an obstacle to adoption as it is difficult to convince users to transfer their money into a non-interest-bearing account.